This post walks step-by-step through a case study that estimates the tax impact of exercising startup stock options.

I made this for myself, so I figured I’d share. It’s long and boring, but also possibly helpful.

Lawyer warning: Before you do anything, talk to a professional! This is a high-level summary to give you an idea of how the system works, not a way to calculate your taxes. Do not rely on this to do anything!

I hope this is helpful to someone! Please tweet at me or email me if you have any feedback or questions about startup law, finance, or operations. Happy to write more like this if helpful.

TL;DR

If you just want a super quick, very rough estimate of your potential taxes, and don’t want to read this entire post (I understand!):

- Click here to make a copy of the Google Doc model (you need to be logged into Google).

- Change cells: B2, AC2, AC4, and AC5 and see the results.

The Model

This is the model that Sam, a startup employee living in New York City, built to estimate what her income taxes would be if she exercised her startup options in 2014. You can follow along by making a copy of the sheet and entering your own numbers.

Regular Method versus AMT

You pay the higher of the taxes under the regular method and the Alternative Minimum Tax (AMT) method, so you need to know your taxes under both to know which applies.

The reason this is so important is that under the regular method, you probably have no tax implications of exercising your options. But if the AMT applies, you probably do, and the taxes can be high.

Sam may also have to pay state and local AMT, as in New York and California, but we’re focusing on the much larger federal tax in this post.

Let’s start by calculating Sam’s taxes using the regular tax method.

Regular Tax Method

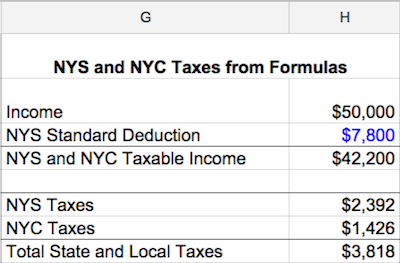

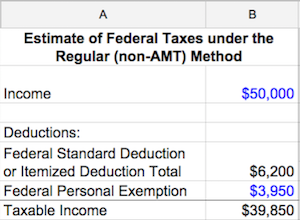

Sam starts with her income. Her salary for 2014 is $50,000. That’s her only source of income. She enters that into cell B2 of the model.

Sam doesn’t have to pay taxes on her full income because the tax law allows credits and deductions.

Sam can either figure out every deduction she has by itemizing her deductions, or she can just use the standard deduction. The IRS says: “Most taxpayers have a choice of either taking a standard deduction or itemizing their deductions. If you have a choice, you can use the method that gives you the lower tax.”

So, Sam calculates both deductions to decide which to use.

Itemized Deductions

Sam calculates the itemized deductions first. She figures out her big itemized deductions: state and local income taxes. The government allows lots of other deductions, but those either don’t apply to Sam or are too small to affect her decision on whether to exercise her options.

In columns G to H of the model, Sam uses the New York State instructions to estimate her state and local taxes.

For her state and local taxes, just like her federal taxes, Sam can itemize her deductions or take the standard deduction, and choose the method that lowers her taxable income more. Sam has no substantive deductions to itemize for her state and local taxes so she’ll take the standard deduction.

Page 18 of the instructions tell her the standard deduction is $7,800.

That gives her a taxable income of $42,200 in cell H4.

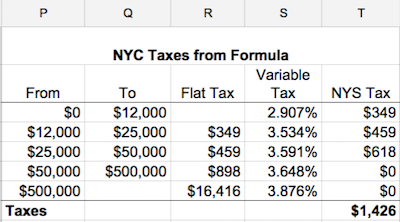

Sam then creates the tables in columns J to T of the model to calculate her state and local taxes.

In columns J to N of the model, Sam uses the formula on page 50 of the instructions to calculate her state taxes of $2,392.

In columns P to T of the model, Sam uses the formula on page 62 of the instructions to calculate her city taxes of $1,426.

Those instructions also have tax tables, on pages 42 and 54, to look up your taxes if you want to double check the spreadsheet.

Using those formulas, Sam comes up with a total of $3,818 in total tax due to New York State and City, which also is the itemized deduction she can take.

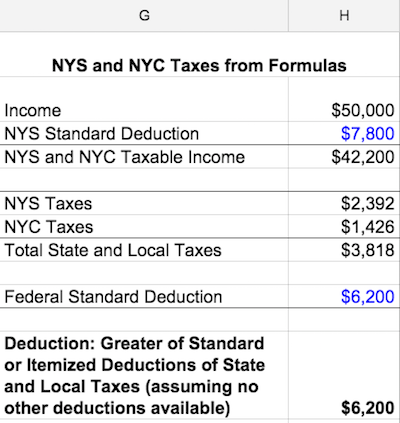

She now has to compare the itemized deductions total of $3,818 to her federal standard deduction to decide whether to take the itemized deductions or standard deduction.

Standard Deduction

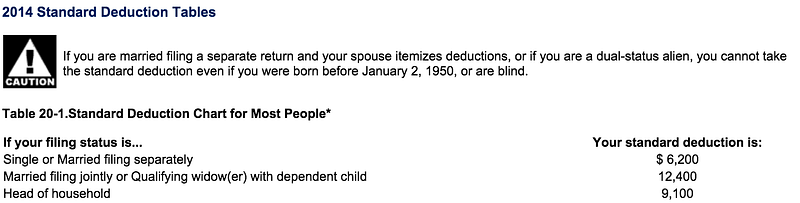

Sam looks up her standard deduction in the table. Sam’s standard deduction would be $6,200.

She enters that number into cell H10. Cell H12 of the spreadsheet tells her to take the $6,200 standard deduction because it’s greater than the itemized deduction of $3,818.

Personal Exemption

She can deduct one more number, her personal exemption of $3,950, from her federal taxable income before calculating her taxes.

In cell B7, Sam deducts $3,950 for her personal exemption and gets a taxable income of $39,850 in cell B8.

Now that she has her taxable income, she’s ready to calculate her federal taxes.

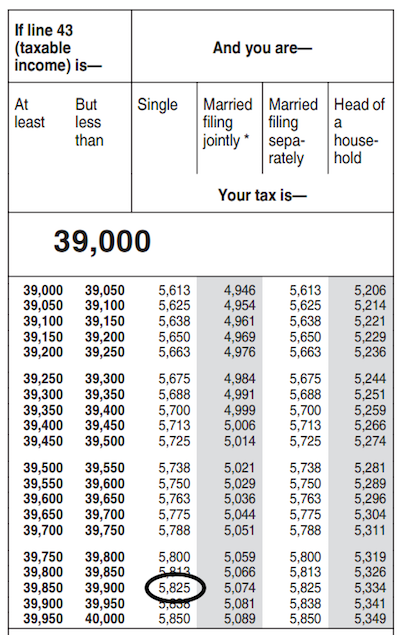

In columns V to Z of the model, Sam uses the formula and page 81 of the tax tables (more detail here and here), to calculate her federal taxes of $5,819 in cell Z10, which the spreadsheet automatically puts in B10. (The tax tables are a few dollars more because they aren’t exact.)

AMT Method

Sam now has to calculate her taxes under the AMT method, so she can compare her taxes under both methods and choose the one that provides the lower tax bill.

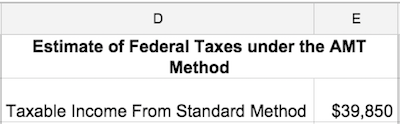

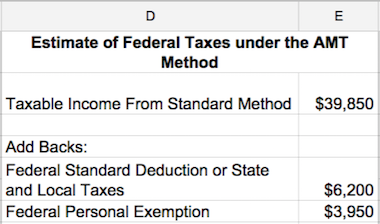

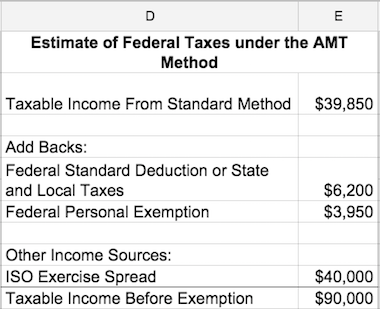

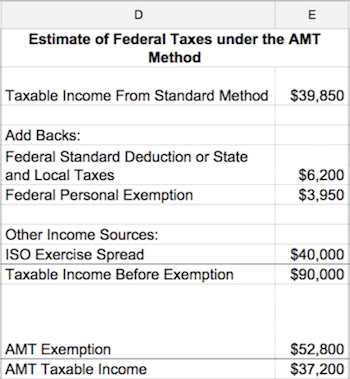

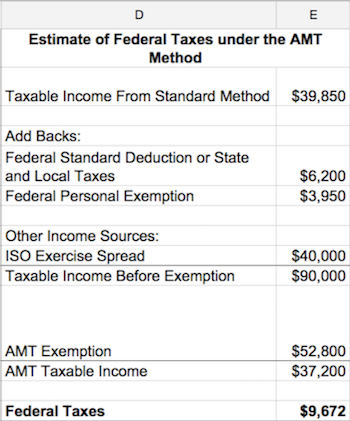

In columns D and E, Sam calculates her taxes under the AMT. Sam starts with her taxable income from the regular method, $39,850 in cell E2.

The AMT form tells her to add back to that amount certain deductions from the regular tax calculation.

The only deduction Sam took was the standard deduction, so she adds back that and the federal personal exemption.

Sam next has to add in certain other sources of taxable income.

The AMT instructions say that Sam must include any gain from exercising her stock options (most startups grant Incentive Stock Options, ISOs for short, because of better tax treatment than other versions), so she must add in the difference in value between the exercise price and fair market value at time of exercise.

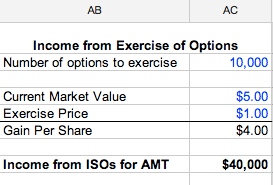

In columns AB to AC, Sam calculates her ISO gain. She’s vested 10,000 options, each with a current market value of $5 and an exercise price of $1. (You should be able to ask your company for each of those numbers.) She multiplies the 10,000 options times the difference in price of $4 to get $40,000.

That income automatically populates cell E10 as the ISO exercise spread. That gives her an income of $90,000 for the AMT method.

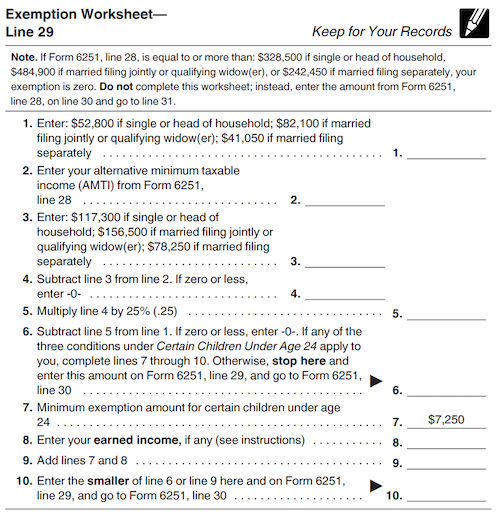

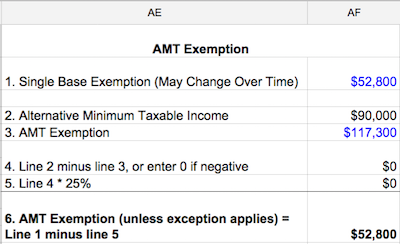

In columns AE to AF, Sam then calculates her AMT exemption, using the form on page 9 of the instructions.

As the note at the top of the form says, if Sam’s income were at least $328,500, she’d receive no exemption. Sam’s income isn’t that high, so she continues with the calculation in columns AE to AF.

That exemption amount automatically goes into cell E12. She now has all the inputs to figure out that her taxable income under the AMT is $37,200.

Sam’s ready to figure out her taxes under the AMT method using the formula on line 63 of the IRS AMT form. In IRS language: “If line 36 is $182,500 or less ($91,250 or less if married filing separately), multiply line 36 by 26% (.26). Otherwise, multiply line 36 by 28% (.28) and subtract $3,650 ($1,825 if married filing separately) from the result.”

Using this formula in cell E15, Sam estimates her federal taxes under the AMT calculation to be $9,672.

That compares to $5,819 under the regular method. You can see the difference of $3,853 in cell B18. So, if she exercise, she’ll be stuck paying the higher AMT tax amount.

Make a Decision

She can now decide whether to exercise her options. If she has the extra money to pay the taxes (and can cover the exercise cost, which would be the exercise price of $1 times the number of options 10,000 if she wants to exercise all of them, so that’s a lot of money!), she may want to do it. The two main benefits of exercising sooner are:

- Starting the clock on long-term capital gains tax rates which are lower than regular income tax rates.

- The AMT impact becomes even greater as the company’s valuation rises. As cell AC4 in the model goes up and the exercise price remains the same, the taxable income from the options goes up.

The valuation could also drop, even to zero, so exercising is a risk!

AMT Credits

Sam also may get future tax credits for paying the AMT. So, that difference between the tax paid under the AMT and regular methods might come back to her over time.

Like the AMT itself, the law around AMT credits is complicated and unpredictable. Here are a few articles explaining it (notice the dates on these, and make sure they’re up to date): SmartMoney, Fairmark, MyStockOptions.

Be Careful!

In conclusion, BE CAREFUL when deciding whether to exercise your options. You might end up with a tax bill and no cash to pay it! Seek professional assistance, and do your own research!

Hope this was helpful to someone! Please tweet at me if you have any comments, I’d love to hear them and improve this if you have feedback.

If you’re also interesting in figuring out the value of your startup options, this other blog post might help.

Hacker Noon is how hackers start their afternoons. We’re a part of the @AMI family. We are now accepting submissions and happy to discuss advertising & sponsorship opportunities.

If you enjoyed this story, we recommend reading our latest tech stories and trending tech stories. Until next time, don’t take the realities of the world for granted!